The Bank of Canada Increases Interest Rates Yet Again

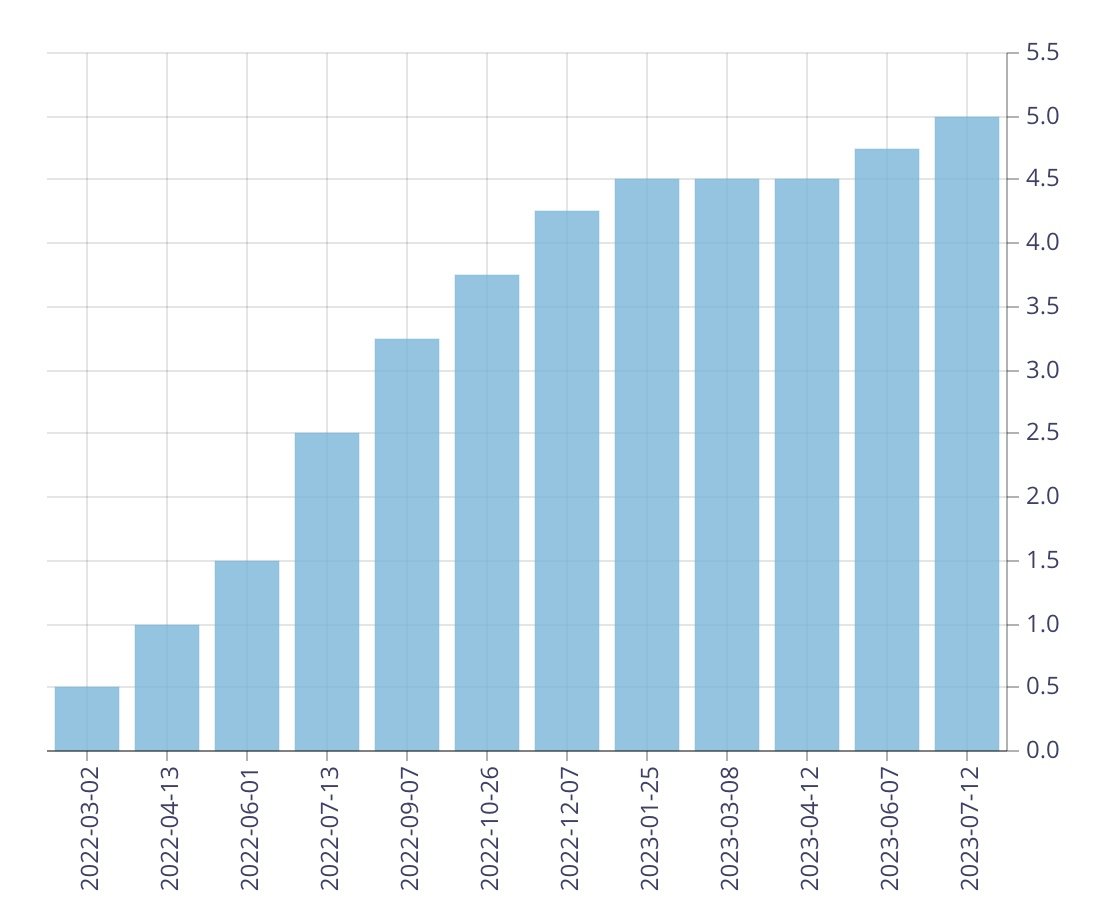

On July 12, 2023, the Bank of Canada raised its target for the overnight rate by 0.25%, bringing it to 5.00%, making the cost of borrowing more expensive. The central bank has been steadily increasing interest rates as an effort to combat inflation. This increase marks the 10th rate hike since March 2022.

Omar Hashem of Lotful Realty says he believes this rate hike will reduce demand while prices may stay stable.

“Throughout certain areas of Ottawa, property values experienced a notable 5-10% upswing, coinciding with a 0.5% decrease in fixed interest rates. Although this surge was relatively short-lived in 2023, it clearly indicates a heightened demand driven by the more favorable interest rates available to buyers,” says Hashem.

“Amidst the anticipation of potential rate increases by the Bank of Canada, the real estate market is witnessing a plateau in prices. While this might lead to a temporary reduction in demand, the summer season brings its own seasonal changes,” said Hashem.

He continued by saying that we can expect the market to regain momentum in the fall, especially as economic data solidifies the impact of previous interest rate hikes. The real estate landscape remains dynamic, adapting to changing circumstances.

Policy Interest Rates, Recent Data from the Bank of Canada

This rate increase typically impacts variable rate mortgage holders and influences the amount of money people pay when borrowing from banks for loans or mortgages.

When the benchmark interest rate goes up, banks will also increase their prime rates. The prime rate is the interest rate banks charge their most trustworthy customers.

The Bank of Canada’s July Monetary Policy Report (MPR) provides projections for global economic growth, indicating positive trends in the coming years. The Bank’s July Monetary Policy Report (MPR) projects the global economy will grow by 2.8% this year and 2.4% in 2024, followed by 2.7% growth in 2025.

Canadian economic growth has historically been strong, and despite the pandemic-induced downturn, the country has experienced a rapid recovery.

The combination of increased immigration and a growing population has played a significant role in fueling this recovery. As a result, these factors have major impacts on both the housing market and consumer spending in general or all other sectors. According to StatCan, shelter accounts for 28 per cent of the CPI basket weight and food accounts for 16 per cent. As a result, drastic changes in these two components can heavily influence inflation rates.

TD Bank says the increasing number of households, due to immigration, in Canada has provided a significant boost to the domestic economy. This increase in demand and labor supply has contributed to Canada’s economic resilience, “even amidst the Bank of Canada's aggressive tightening measures,” according to TD Bank.

TD Bank noted, “Economic growth does not necessarily equate to economic prosperity.”

Canada’s unemployment rate rose to 5.4 per cent in June; however this number is still below the pre-pandemic average of 5.7 per cent, indicating ongoing recovery. The Bank of Canada wants the unemployment rate to return to the pre-pandemic average. Unemployment plays a crucial role in stabilizing wages. When there is a certain level of unemployment, it helps create a balance in the labor market. Maintaining this level of unemployment can help keep wages in check and prevent a vicious cycle of rising costs and inflation trends.

According to the Bank of Canada, the next scheduled date for announcing the overnight rate target is September 6, 2023.

Rest assured, Lotful Realty is here to provide guidance and support during these times. We can often tailor a solution for you with one of our lending partners. If you have any questions or concerns about how these rate increases may affect you, do not hesitate to contact us.